If you follow technology news, startup booms can feel chaotic. One year everyone is launching crypto companies, the next it's AI, climate tech, or biotech. Venture funding surges, founders appear everywhere, and then, inevitably, the hype cools down.

It can look like randomness. But research in economics and innovation studies suggests something else: startup booms are a natural phase of technological evolution.

For scientists thinking about turning research into real-world impact, understanding these cycles is extremely useful. It helps explain when opportunities appear, why experimentation explodes at certain moments, and why many startups fail while a few reshape entire industries.

Innovation doesn't happen smoothly

We often imagine technological progress as a steady line. New discoveries accumulate gradually and the economy improves step by step. In reality, innovation behaves more like a series of waves.

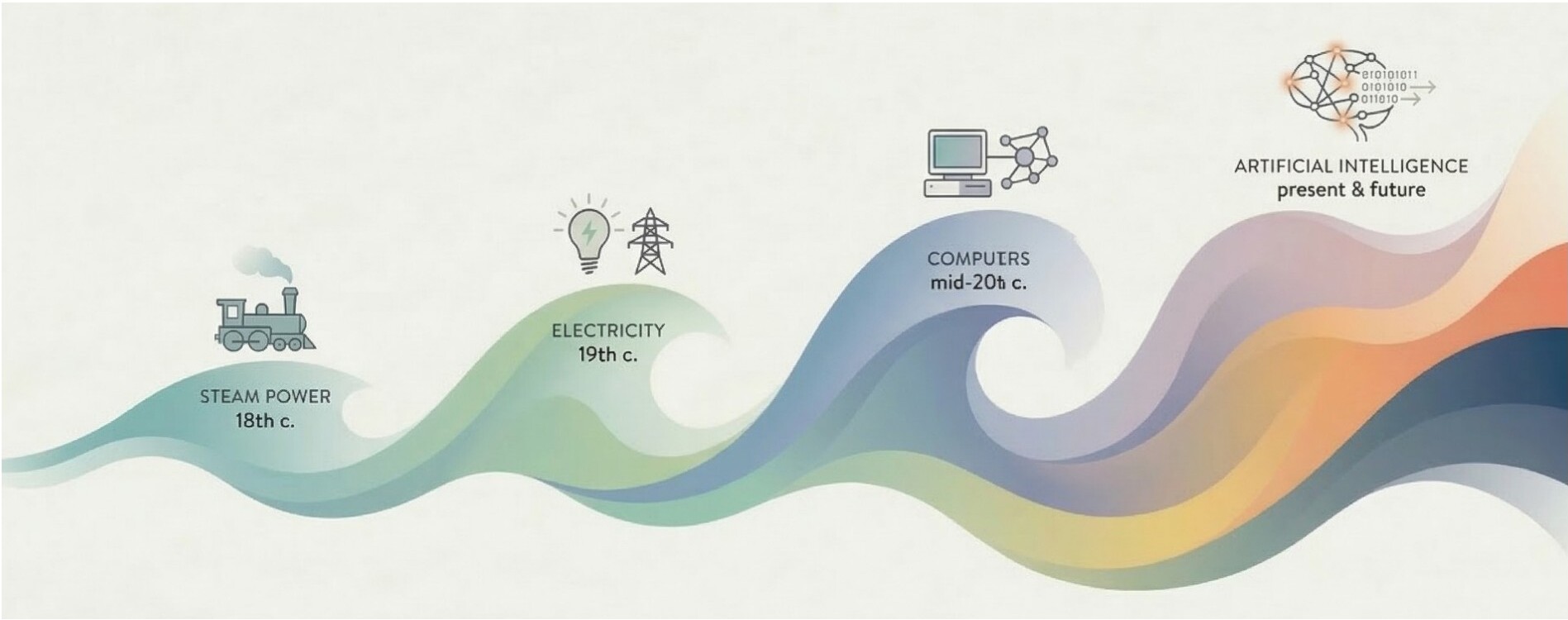

New technologies tend to appear in clusters. When a breakthrough occurs, it often triggers a cascade of related inventions and applications. Entire families of industries can emerge from a single technological foundation. Railways grew from steam power, electrification enabled mass manufacturing, and digital computing gave rise to the internet and modern software ecosystems.

Economic historians have long suggested that these technological revolutions unfold in long cycles that can span several decades. Each wave begins with a handful of breakthroughs and eventually transforms entire sectors of the economy. Startup booms tend to appear right at the beginning of these waves, when a new technology suddenly creates many unexplored possibilities.

The hidden mechanics of innovation waves

One way to understand these cycles is to think of innovation as unfolding in two layers. The first consists of primary innovations: fundamental technological breakthroughs such as artificial intelligence, genome sequencing, or the internet itself. The second consists of secondary innovations: the applications that use those breakthroughs to build real products and services: recommendation systems, self-driving vehicles, telemedicine platforms, or new biotechnology therapies.

When a new foundational technology appears, researchers and companies initially know very little about how to use it. But over time, they learn. Engineers experiment, tools improve, and knowledge spreads across industries. This process creates what economists often describe as a learning-by-doing effect. As people gain experience working with a technology, productivity rises and innovation accelerates.

Eventually, however, progress slows. The most obvious ideas have already been explored, and new discoveries become harder to find. Economists sometimes call this the fishing-out effect: as the pool of easy ideas shrinks, the pace of innovation declines. At that point, the cycle begins to wind down until a new foundational breakthrough appears and the process starts again.

Why venture capital suddenly loves risk

Technology alone doesn't explain startup waves. Money matters too. Venture capital markets also move in cycles, and those cycles influence the kinds of startups that receive funding.

During periods when investment capital is abundant, investors tend to fund more unusual and experimental ideas. With more money available, the cost of trying new things falls. Investors can afford to support projects that might fail but could also produce significant breakthroughs.

As a result, startups funded during these periods often sit at the extremes. Many fail. But those that succeed frequently generate major technological advances, valuable intellectual property, and entirely new markets. In this sense, funding booms create conditions for large-scale experimentation.

The creative destruction engine

Innovation does not simply add new industries to the economy. It also replaces existing ones. More than eighty years ago, economist Joseph Schumpeter described capitalism as a process of creative destruction. New technologies continually disrupt established industries, transforming the economic landscape from within.

Historical evidence supports this pattern. When countries develop new technological capabilities, they often begin producing clusters of new products. At the same time, older industries gradually decline as newer, more sophisticated technologies take their place. Innovation, in other words, is not only creative. It is also transformative.

Where startups fit in

Startups play a special role in this process. Unlike established companies, startups are designed to operate under extreme uncertainty. Their purpose is not simply to build products, but to search for scalable and repeatable business models around emerging technologies.

Because of this, startups move quickly. They experiment with new approaches, pivot when early assumptions fail, and adapt as they learn more about the market. This rapid experimentation comes with risk. Many startups fail, often because the technology, market, or timing is not quite right. But a few succeed, and those successes can reshape entire industries.

What this means for scientists

For scientists considering entrepreneurship, startup booms are not just moments of hype. They are signals that a new technological wave may be forming. These waves usually emerge when three forces align:

- A major scientific or technological breakthrough

- Investors willing to fund experimentation

- Networks of talent, infrastructure, and early adopters

When these conditions come together, experimentation accelerates. Thousands of teams begin exploring the possibilities of a new technology at once. Most of those experiments will fail. But collectively, they help society discover how a new technology can reshape the world.

Seen from this perspective, startup booms are not chaos. They are how innovation learns.